Every Quote Is Free & Confidential

Every Quote Is Free & Confidential

The credit crunch left a lot of us with some residual bad credit, or a little overstretched and even now some people have had hiccups on their credit record, we are aware of this issue and so try to add products to our loan selection to cover customers with Good, Fair and even Adverse or Poor credit.

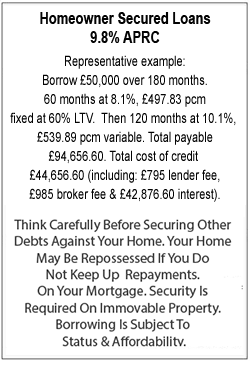

The credit crunch left a lot of us with some residual bad credit, or a little overstretched and even now some people have had hiccups on their credit record, we are aware of this issue and so try to add products to our loan selection to cover customers with Good, Fair and even Adverse or Poor credit. Borrowing money with a homeowner loan can be an effective way to obtain some larger amounts of finance on a decent interest rate and give you the ability to spread the payments over a long or short period of time. The minimum you can borrow is £5,000 and the shortest time you can take it out over is 3 years, or 36 months. However you can pay the loan back early at any time if you are able and will normally just pay one or two months interest plus the capital outstanding. At the other end of the scale loans for homeowners can be as large as £200,000 and repayment periods can go to as long as 25 years to suit your cash flow. As a matter of interest our most popular homeowner loans range between £15,000 and £35,000 with a term of around 7 to 9 years

Borrowing money with a homeowner loan can be an effective way to obtain some larger amounts of finance on a decent interest rate and give you the ability to spread the payments over a long or short period of time. The minimum you can borrow is £5,000 and the shortest time you can take it out over is 3 years, or 36 months. However you can pay the loan back early at any time if you are able and will normally just pay one or two months interest plus the capital outstanding. At the other end of the scale loans for homeowners can be as large as £200,000 and repayment periods can go to as long as 25 years to suit your cash flow. As a matter of interest our most popular homeowner loans range between £15,000 and £35,000 with a term of around 7 to 9 yearsSecured homeowner loans

Video transcript

If you have not found a lender to give you enough money for the purposes you need it for, or won`t sanction a loan based on your borrowing history, you may want to look into secured homeowner loans.Your intention may be to spend tens of thousands of pounds on a major project like redeveloping your home with a view to increasing its value or to improve your living standards and in the current climate homeowners may find it difficult to get these projects of the ground.

On the other hand, you may be looking to reorganise your unsecured debts or credit cards and loans into a single secured home loan, which will be easier to keep track of and should require much smaller monthly payments.

However, if the homeowner loan is paid over a longer period, you may incur more interest costs in total over the term.

Of course, most of us are not aiming to borrow an extravagant amount of money, just enough to get your project completed. If you are a homeowner and interested in a secured loan, even if you have a lack of credit history or you are self employed , you may still be able to get those funds sorted from First Choice Finance.

The same goes even if you are unlucky enough to have an impaired credit history.

With this kind of borrowing, your property is used as security so that the lender can see your level of commitment to repaying the loan and there appears to be a growing trend towards granting loans secured against property, with the Bank of England`s Credit Conditions Survey showing that availability increased over the fourth quarter of 2012.

If you`re interested in finding out more about secured homeowner loans, fill in our short on line form at firstchoicefinance.co.uk or speak to one of our finance advisers on 0800 298 3000 from a landline or 0333 003 1505 from a mobile for a free quote.